Cargo Owners' Legal Liability Explained

Cargo owners legal liability explained: when cargo owners face third-party claims and how liability cover differs from cargo insurance.

Cargo Owners' Legal Liability: When Your Cargo Damages the Vessel and You Owe More Than the Cargo Was Worth

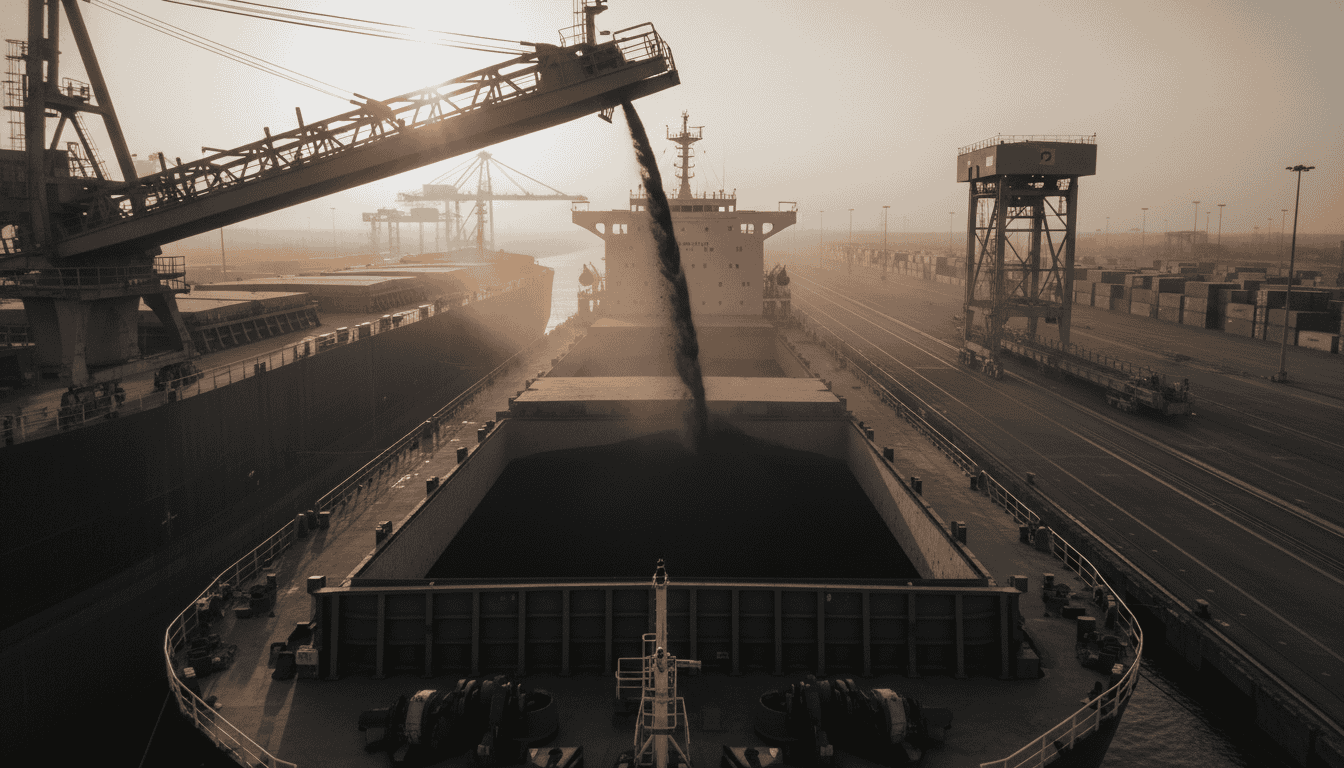

A bulk carrier loads a parcel of coal at a Southeast Asian terminal. Mid-voyage, the cargo self-heats. The temperature in the hold rises past the ignition point of methane evolved from the cargo and a fire takes hold. The vessel is damaged. Adjacent cargo is destroyed. Salvage is engaged. Pollution response is mobilised. The cargo owner's loss is the coal itself, perhaps a few hundred thousand dollars. The cargo owner's liability is to the shipowner, the cargo interests in adjacent holds, the salvors, and any pollution response, and that bill can run into the tens of millions.

This is the gap most cargo owners do not know they have. Cargo insurance protects the cargo. It does not protect the cargo owner against what the cargo does to other things. The product that responds is cargo legal liability cover, structurally part of marine liability rather than marine cargo, and the trader who has not bought it can be in a fight they had not budgeted for.

The legal mechanism, in plain language

A cargo owner can be liable to multiple parties when their cargo causes harm. The shipowner has a claim under the contract of carriage and in tort if cargo properties cause damage to the vessel. Other cargo interests in the same vessel have a claim where their cargo is damaged by yours. Terminal operators have a claim where the cargo damages handling equipment, infrastructure, or other cargo at the terminal. Pollution response authorities have statutory claims for cleanup costs in many jurisdictions.

The Hague-Visby Rules, often misunderstood as protecting the cargo owner, actually limit the carrier's liability to the shipper (SDR 666.67 per package or 2 SDR per kg, whichever is higher, requiring the shipper to prove carrier fault). They do not limit the shipper's or cargo owner's liability to the carrier or other parties when the cargo is the cause of harm. The flow runs in both directions and the shipper-side limits do not apply to it. For the full carrier-liability picture across sea, air, road, and rail conventions, see carrier liability limits.

P&I clubs covering shipowners, members of the International Group's 12 clubs (post-2024 merger) covering approximately 90 percent of world ocean-going tonnage, will pay the shipowner for damage caused by cargo, then exercise rights of subrogation against the cargo owner. The cargo owner's defence to the subrogation claim is either (a) the cargo did not cause the damage, (b) the loss falls within an exception (force majeure, properly declared peril of the sea), or (c) the cargo legal liability cover responds and pays the claim subject to its terms.

Resource: Cargo Owners Legal Liability Awakening Card

Download the Cargo Owners Legal Liability Awakening Card for a one-page reference for the four scenarios cargo owners often miss. Designed for finance and risk teams. Free, no signup wall.

The four cargo owner liability scenarios that actually generate claims

Scenario 1: Self-heating coal damages a vessel

Coal cargoes are listed in the IMSBC Code (International Maritime Solid Bulk Cargoes Code) as Group B (cargoes which possess a chemical hazard which could give rise to a dangerous situation on a ship). Self-heating is a recognised hazard. When the cargo's actual properties exceed what was declared (higher moisture, higher sulphur, higher coal-rank), the self-heating risk rises and a fire becomes more likely. Our cargo-specific treatment for the commodity is in coal cargo insurance.

The shipowner's claim against the cargo owner sits on three legs: misdeclaration of cargo properties (a contractual breach under the bill of lading), failure to comply with IMSBC Code requirements (a statutory breach in many jurisdictions), and damage to the vessel and other cargo (a tort and contractual claim). Cargo legal liability cover responds to defence costs and indemnity, subject to policy terms and conditions.

Scenario 2: Contamination spreads to adjacent cargo

A vessel carries multiple commodity parcels in different holds or tanks. One cargo's properties (oils leaking through a hatch cover, gas evolution from a chemical cargo, water damage from a damaged drum spreading) cause damage to adjacent cargo. The other cargo interests claim against the carrier; the carrier's insurer subrogates against the cargo owner whose cargo was the cause.

This pattern is common in bulk and break-bulk operations. The cargo owner's exposure is to the value of the adjacent cargo, plus salvage charges, plus consequential delay claims if the contamination disrupts the voyage schedule. Cargo legal liability extends to these claims, subject to policy terms and conditions.

Scenario 3: Mis-declared dangerous goods cause a fire or explosion

The IMDG Code (International Maritime Dangerous Goods Code) classifies dangerous goods into nine classes and prescribes packing, labelling, and stowage requirements. Mis-declaration (declaring lithium batteries as "consumer electronics", declaring fireworks as "general merchandise", under-declaring DG quantities to avoid surcharges) is a recurring cause of vessel fires. Container ships, in particular, have suffered multiple major fires in the past decade traceable to mis-declared DG.

The cargo owner's liability when mis-declared DG causes harm is broad and not easily limited. Defence costs alone can run into millions for a serious incident. Cargo legal liability cover is the principal product responding, but the policy will scrutinise carefully whether the cargo was declared honestly; willful misconduct of the assured (Clause 4.1 of ICC (A) 2009 in the cargo policy, similar wording in liability policies) is excluded.

Scenario 4: Packaging failure causes third-party damage

A flexitank ruptures in a container yard, oil spreads, the terminal incurs cleanup costs, adjacent containers are contaminated, and the terminal's claim against the carrier flows back to the cargo owner via subrogation. A pallet of liquid drums fails on a truck, contaminating the road and adjacent vehicles. Lashing fails on deck cargo, the cargo damages other parcels.

The cargo owner's liability here turns on whether the packaging was specification-correct and properly fitted, or inadequate. Cargo legal liability responds to claims arising from packaging failure, subject to the assured's compliance with declared packing standards and the policy's specific exclusions.

Why your marine cargo policy does not respond to this

ICC (A) 2009 covers physical loss or damage to the cargo subject to the policy terms and conditions. The cargo is the subject matter insured. What the cargo does to other things is outside the cargo policy entirely; it is a liability matter, not a property matter.

The standard cargo policy carries no third-party liability section, no defence costs cover for claims by third parties, and no subrogation indemnity to respond to a shipowner's P&I subrogation claim. The cargo owner's claim under the cargo policy is for the cargo's value (subject to the sum insured); their liability exposure is uninsured under that policy alone.

| Loss | Cargo policy (ICC (A)) | Cargo legal liability |

|---|---|---|

| Damage to your own cargo (vessel sinks) | Responds, subject to policy terms and conditions | Does not respond |

| Your cargo damages the vessel | Does not respond | Responds to defence and indemnity, subject to policy terms and conditions |

| Your cargo contaminates adjacent cargo | Does not respond | Responds, subject to policy terms and conditions |

| Mis-declared DG causes fire | May not respond if mis-declaration breaches policy warranty | May respond if mis-declaration was negligent, not willful, subject to policy terms and conditions |

| Pollution from packaging failure | Does not respond to third-party pollution claims | Responds, subject to pollution sub-limit and policy terms and conditions |

Where the liability gap sits between cargo insurance and Hull/P&I

The shipowner carries Hull and Machinery for damage to their vessel and Protection and Indemnity for third-party liabilities (crew, cargo claims, pollution, wreck removal, 1/4 collision liability). When the cargo is the cause of damage, the shipowner's H&M and P&I respond to the shipowner's losses; the P&I club then subrogates against the cargo owner who is the legal cause.

The cargo owner sits on the receiving end of that subrogation. Without cargo legal liability cover, the cargo owner pays the subrogation claim from working capital, or fights it in court. With cargo legal liability cover, the policy responds to defence and indemnity within its terms.

The Marine Liability money page on our site covers the broader product family; cargo legal liability is one of several cover types in the marine liability suite, alongside Freight Forwarder's Liability, Terminal Operator's Liability, and Ship Repairer's Liability. Each addresses a different actor in the chain. Cargo legal liability addresses the cargo owner specifically.

How to size and structure the cover

Three structural decisions matter at placement.

Limit per voyage. The right limit reflects the worst plausible loss the cargo could cause, not the cargo's own value. A USD 200,000 parcel of mis-declared DG can cause a USD 100 million vessel fire; the limit should be sized against the latter, not the former. For most container shippers and bulk traders, limits in the USD 5 million to USD 50 million range are common, with the upper end driven by route, commodity, and vessel type.

Aggregate limit. The annual aggregate caps the policy's total payout across all voyages in the policy year. Set too low, the cover exhausts on the first major incident; set realistically, it provides defence and indemnity capacity across multiple events.

Pollution sub-limit. Pollution response is a defined exposure with its own limits. Some policies sub-limit pollution within the overall limit; some require a separate pollution cover. For dangerous goods exporters and bulk liquid traders, the pollution sub-limit is often the binding constraint at claim.

Defence costs. Defence costs (legal and expert fees to defend the claim) can run into millions before any indemnity is paid. The right structure typically pays defence costs in addition to the limit, not within it; this is worth confirming explicitly at placement, subject to policy terms and conditions.

Frequently asked questions

Does my cargo insurance cover damage my cargo causes?

No. ICC (A) 2009 cargo cover responds to damage to the cargo, not to damage caused by the cargo. The product that responds to damage caused by the cargo is cargo legal liability cover, a separate placement under the marine liability product family, subject to policy terms and conditions.

Who pays if my dangerous goods cause a fire?

If the DG was correctly declared and packed, the carrier's loss is generally allocated through general average and recovered from cargo and Hull/P&I in proportion. If the DG was mis-declared, the cargo owner is liable for the full loss including defence costs, and cargo legal liability cover is the principal responding product, subject to policy terms and conditions.

What is the difference between cargo legal liability and freight forwarder's liability?

Cargo legal liability protects the cargo owner against claims by third parties whose property or interests are damaged by the cargo. Freight Forwarder's Liability protects the freight forwarder against claims by cargo owners (and others) for loss or damage to cargo in the forwarder's care. They are bought by different parties for different exposures.

Do I need this if I ship under FOB?

Often yes, because the cargo is your cargo until on-board moment under FOB and your liability for what it does in the pre-loading window is yours. After on-board, the legal exposure remains yours in many jurisdictions because the cargo is still your goods even if the risk to the goods has transferred. The right answer depends on your sale contract and your jurisdiction.

Does general average cover this?

No. General average is the maritime law principle (governed by the York-Antwerp Rules, most recent revision 2016, with 2004 rules still widely incorporated) under which all cargo and the vessel contribute proportionally to a voluntary sacrifice for the common safety. It allocates loss; it does not extinguish liability for the cargo owner whose cargo was the cause of the incident.

Can I be sued personally as a director?

In some jurisdictions, yes, particularly where personal misconduct is alleged (knowing mis-declaration of DG, knowing breach of IMSBC Code requirements). Cargo legal liability covers the assured (typically the cargo-owning company); directors' personal exposure is a separate question best raised with legal counsel, subject to policy terms and conditions.

Voyage Conclusion

Cargo owners often discover this exposure for the first time when the shipowner's lawyers send a subrogation letter after a major incident. By then, the insurance question is whether cargo legal liability cover was placed before the voyage. Without it, the cargo owner pays from working capital. With it, the policy responds to defence and indemnity within its terms.

Talk to Voyage about Marine Liability Insurance for Malaysian and Singaporean traders, bulk shippers, and dangerous goods exporters whose cargo can cause loss to a vessel or third party. Pair with Marine Cargo Insurance on the cargo side and Freight Forwarders Liability Insurance on the logistics side. For the corridor-specific industry view, see Commodities & Trading Houses Cargo Insurance. WhatsApp +60 14 925 5243 or use the contact form.

Download the Cargo Owners Legal Liability Awakening Card

Cargo Owners Legal Liability Awakening Card: one-page reference covering the four claim scenarios. Pair it with the Hague-Visby Cargo Recovery Card for the recovery-side maths against your carrier. Free, no signup wall.

Related guides: carrier liability limits and what your shipping line owes, why your freight forwarder is not your insurer, freight forwarder liability insurance, insuring palm oil exports from Malaysia in 2026, coal cargo insurance.

Disclaimer: This article provides general guidance on cargo owners' legal liability and marine liability insurance as of April 2026. Coverage terms, conditions, and availability vary by insurer, policy, and jurisdiction. Regulatory requirements differ between countries and may change. Always review your specific policy wording and consult a qualified insurance or legal professional before making coverage decisions.

Why Voyage

Marine Insurance Specialists

International Underwriter Access

Both Sides of the Supply Chain

Malaysia and Singapore Expertise

Other industries

Explore other industries we cover

Shipping Disruption and Your Cargo Is Stuck: What Your Insurance Covers and What It Does Not

Learn more

Get Best Rates / Quotation

Voyage is a specialist marine insurance intermediary arranging marine cargo and marine liability coverage for businesses in Malaysia, Singapore, and internationally. All insurance is placed through licensed broking partners.

Riskflow Sdn Bhd (202101001225):

Suite 3.19 (North Block), The Ampwalk, 218 Jalan Ampang, 50450 Kuala Lumpur, Wilayah Persekutuan Kuala Lumpur

t: +60149255243 (Kevin H.)

email: kevin@voyagecover.com