What Your Forwarder's Marine Certificate Actually Covers

A look at what an MOC certificate from a forwarder really covers, where the master open cover sets the terms, and how to read what you're holding.

What does the marine certificate your freight forwarder hands you actually cover? Most cargo owners have never read theirs end to end.

The certificate arrives as part of a freight quote, the cargo owner glances at the sum insured figure and the voyage description, and the document goes into a folder. Then a claim happens, and the question becomes urgent.

The conceptual case for not relying on a forwarder for insurance is made elsewhere; Voyage's your freight forwarder is not your insurer covers it in detail. This article is the operational sibling.

You have already bought through your forwarder. The question now is what is on the certificate, what is in the master wording behind it, and how do you tell whether what you are holding is right for your trade.

Key Facts: Forwarder Marine Open Cover Certificate Cover

What is a marine open cover (MOC) certificate? It is a document issued under a master marine open cover policy held by the freight forwarder, evidencing that a specific shipment is covered by that facility. The certificate is the evidence; the substantive contract is the master wording between the forwarder and the underwriter.

Who is the policyholder under a forwarder's MOC? The freight forwarder is the policyholder under the master open cover with the underwriter, and the cargo owner is named as the assured (or as a beneficiary or assignee) for the specific shipment listed on the certificate. The contractual relationship sits between the forwarder and the underwriter; the cargo owner's rights flow through the certificate, subject to the master wording.

What cover form does an MOC typically reference? An MOC will be written on a specified marine cargo policy form, and the certificate face will reference that form. Common forms in the Malaysian and Singapore markets include Institute Cargo Clauses (A), (B), or (C) 2009 published by the International Underwriting Association, often combined with Institute Standard Conditions for Cargo Contracts dated 01/04/1992 and one or more paramount exclusion clauses.

Where do the limits and exclusions sit? The certificate face usually states the sum insured, named conveyance, voyage description, and ICC version.

The fuller terms (commodity exclusions, sub-limits, vessel age limits, war and strikes scope, geographic restrictions, claims handling protocols) sit in the master open cover wording behind the certificate, which most cargo owners never see. Subject to policy terms and conditions.

What cancellation provisions are typical? Cancellation provisions vary by wording, but a common Malaysian-market pattern allows mutual cancellation on 14 days' notice in writing, with shorter notice for war (typically 7 days) and strikes (typically 7 days, or 48 hours for shipments to or from the United States), reflecting the cancellation provisions in the Institute War Clauses (Cargo) CL385 dated 01.01.2009 and Institute Strikes Clauses (Cargo) CL386 dated 01.01.2009.

For the conceptual treatment of why the forwarder is not your insurer, see your freight forwarder is not your insurer. For the standalone alternative, see marine cargo open cover. For the LC use case where MOC certificate language commonly fails, see LC insurance certificate requirements.

What an MOC Certificate Is, Operationally

A marine open cover is a standing facility between an insurer and a policyholder, under which a portfolio of qualifying shipments is automatically covered for the policy year, with declarations made periodically. When the policyholder is a freight forwarder, the forwarder uses the facility to provide cover on shipments their clients hand them. Each cargo owner is issued a certificate naming the specific shipment, the assured, the sum insured, the voyage, and the cover form referenced.

The certificate is not the policy. The policy is the master wording between the forwarder and the underwriter. The cargo owner's rights under the certificate are derivative of that master wording.

Three structural points follow from that.

First, the cover terms are negotiated at the master cover level, not on the individual certificate. The forwarder agreed those terms with the underwriter when the master cover was placed, typically rated against the forwarder's overall portfolio of cargo and the forwarder's claims experience. The cargo owner inherits those terms by holding a certificate, but did not negotiate them and usually did not see them.

Second, the certificate face does not contain the exclusions and limits. It contains the shipment-specific facts and a reference to the master wording. Exclusions, sub-limits, restricted commodity lists, deductibles, war and strikes scope, vessel age limits, and claims protocols all sit in the master wording behind it.

Third, the master wording is rarely shared with the cargo owner. The cargo owner can usually ask for it. Whether the forwarder shares it is up to the forwarder.

A Worked Example: What a Typical Malaysian-Market MOC Wording Contains

To make the structural points concrete, this section walks through what a typical Malaysian-market MOC wording contains. The clauses and provisions described here are drawn from standard marine open cover wordings used in the Malaysian market and are representative of the structure most cargo owners will encounter. Other insurers' wordings vary materially.

The point is to illustrate what is typically in the master document, not to suggest every MOC reads the same way.

The cover form is set at the time of shipment

A typical MOC master wording is issued subject to the clauses and conditions of the insurer's marine cargo policy form in use at the time of shipment or despatch, plus the clauses and conditions specified in the open cover itself. That single line carries weight.

The cover form (ICC (A), (B), or (C)) is set in the marine cargo policy form referenced at the time of shipment, not in the open cover document itself. The certificate has to state the form for the cargo owner to know what they have.

The master wording incorporates several Institute clauses

A typical Malaysian-market MOC wording explicitly incorporates Institute Standard Conditions For Cargo Contracts dated 01/04/1992, the Institute Classification Clause dated 01/01/2001, the Institute Radioactive Contamination, Chemical, Biological, Bio-Chemical and Electromagnetic Weapons Exclusion Clause dated 10/11/2003, the Institute Cyber Attack Exclusion Clause dated 10/11/2003, and a Termination of Transit Clause (Terrorism). Each of these is a paramount clause in its own right, meaning it overrides anything in the cover that is inconsistent with it.

The CBRN exclusion paramountly excludes any nuclear, radioactive, chemical, biological, bio-chemical, or electromagnetic weapon loss. The Cyber Attack exclusion paramountly excludes loss directly or indirectly caused by use of a computer system as a means of inflicting harm (subject to a narrow carve-back where the policy covers war risks and the computer is part of a weapon's launch or guidance system). These are standard market clauses and appear unconditionally on every shipment under a typical master cover.

Vessel age and classification limits

The Institute Classification Clause 01/01/2001 (incorporated into a typical MOC master cover) applies the marine transit rates only to cargoes carried by mechanically self-propelled vessels of steel construction classed with a Classification Society that is a Member or Associate Member of the International Association of Classification Societies (IACS), or a National Flag Society in defined coastal trade. Cargoes on non-classed vessels must be notified promptly to underwriters. The right to cover depends on compliance with that notification obligation.

There are also age limits. Bulk or combination carriers over 10 years, and other vessels over 15 years, attract additional premium subject to defined carve-outs (containerships, vehicle carriers, and double-skin open-hatch gantry crane vessels up to 30 years on an established and regular trade pattern; general cargo vessels on an established trade pattern up to 25 years). For a cargo owner whose forwarder books space on older feeders or non-classed regional vessels, this is the kind of detail that only surfaces in a claim.

Termination triggers for the terrorism extension

The Termination of Transit Clause (Terrorism) in a typical MOC wording sets out specific triggers for terrorism cover. Terrorism cover terminates on the earlier of the following: the transit clause triggers in the policy itself, delivery to the consignee's or final warehouse, delivery to a warehouse used for elective storage or distribution, or for marine transits, 60 days after completion of discharge from the oversea vessel at the final port (30 days for air transits).

Whichever comes first. Storage beyond those windows is outside the terrorism cover.

Cancellation and the war/strikes notice periods

A typical Malaysian-market MOC wording confirms cancellation by either party on 14 days' notice in writing, with risks covered by Institute War Clauses cancellable at 7 days' notice and risks covered by the Institute Strikes Clauses cancellable at 7 days' notice, or 48 hours notice for shipments to or from the United States. Notice runs from midnight of the day issued. Cover already attached on declared shipments before cancellation runs to its natural termination; future shipments are not covered.

Claims and the survey requirement

The "Event of Loss" condition in a typical MOC wording places several duties on the assured. The cargo owner must claim immediately on carriers, port authorities, or other bailees for missing packages, refrain from giving clean receipts where goods are in doubtful condition (except under written protest), examine container seals on delivery, apply immediately for survey by the carrier or bailee where loss is apparent, and give written notice to the carrier within 3 days for non-apparent damage.

The cargo owner must not sign any Average Bond or pay a General Average deposit without the company's prior approval. Immediate notice of loss must go to the Survey Agents named in the certificate.

The "Notification of Claims" condition requires six categories of supporting document: original policy or certificate, shipping invoices, original Bill of Lading or other contract of carriage, survey report or evidence of loss, landing account and weight notes, and correspondence with carriers. The clause states explicitly that "failure to comply with any of these requirements will prejudice any claim." That is a warranty-style obligation, and a cargo owner who does not know the protocol or does not preserve documentation correctly is at risk of having a valid claim defeated on procedure.

Get a comparison quote from Voyage.

If you currently buy cover bundled into your forwarder's freight quote and are not sure how the master wording compares to a policy in your own name, we can quote a marine cargo open cover or single shipment policy on a comparable basis so you can see the structural difference. Contact us via the contact form or WhatsApp +60 14 925 5243.

Where MOC Limits Commonly Bite

Beyond the worked example, there are recurring patterns in MOC wordings that cargo owners should look for on their own certificate.

Sum insured caps per shipment, per conveyance, per location. A master open cover sets maximum limits at the shipment level, the conveyance (vessel, aircraft, land conveyance) level, and the location level. A typical MOC wording makes this explicit: aggregate liability is limited to the per-conveyance and per-location amounts stated in the schedule. A cargo owner whose individual shipment exceeds the per-conveyance cap is over-exposed unless additional cover is bought.

Restricted commodity lists or commodity-specific warranties. Many MOC wordings exclude or attract warranties on specific commodity classes by default. Common targets are used and second-hand machinery, refurbished goods, fragile and breakable items without specified packing, temperature-sensitive cargo without specified handling, hazardous materials, livestock, and bulk parcels of certain commodities. Not every such exclusion appears in the master document itself; many sit in the schedule or in the underlying marine cargo policy form referenced at shipment time.

Which ICC version is referenced. ICC (A) 2009 is all-risks, subject to the named exclusions in Clauses 4 to 7. ICC (B) and ICC (C) are progressively narrower named-perils forms.

A forwarder MOC defaulting to (B) or (C) leaves the cargo owner without theft cover, without water damage cover, and without the all-risks framework on most loss patterns. Voyage's Institute Cargo Clauses guide sets out the differences clause by clause.

Whether war and strikes are included by default. Standard ICC (A), (B), and (C) policies exclude war (Clause 6) and strikes (Clause 7). War and strikes cover is added through Institute War Clauses (Cargo) CL385 and Institute Strikes Clauses (Cargo) CL386.

Some forwarder MOCs bundle these in as standard; others do not. The certificate face should say.

Geographic scope. Some MOCs are written warehouse-to-warehouse (covering the inland legs at both ends), some are written port-to-port, and some restrict cover to specified countries or excluded sanctioned territories. A cargo owner whose factory-to-port leg is uncovered is exposed to a meaningful slice of the loss curve.

Survey and claims protocols. As illustrated above, claims handling under MOC wordings is procedural. The cargo owner must follow specific steps within specific time limits, instructed by named survey agents on the certificate.

Failure to comply prejudices the claim. The forwarder may help with claims handling as a service, but the substantive obligation runs from the cargo owner to the underwriter.

Reading What You Already Have

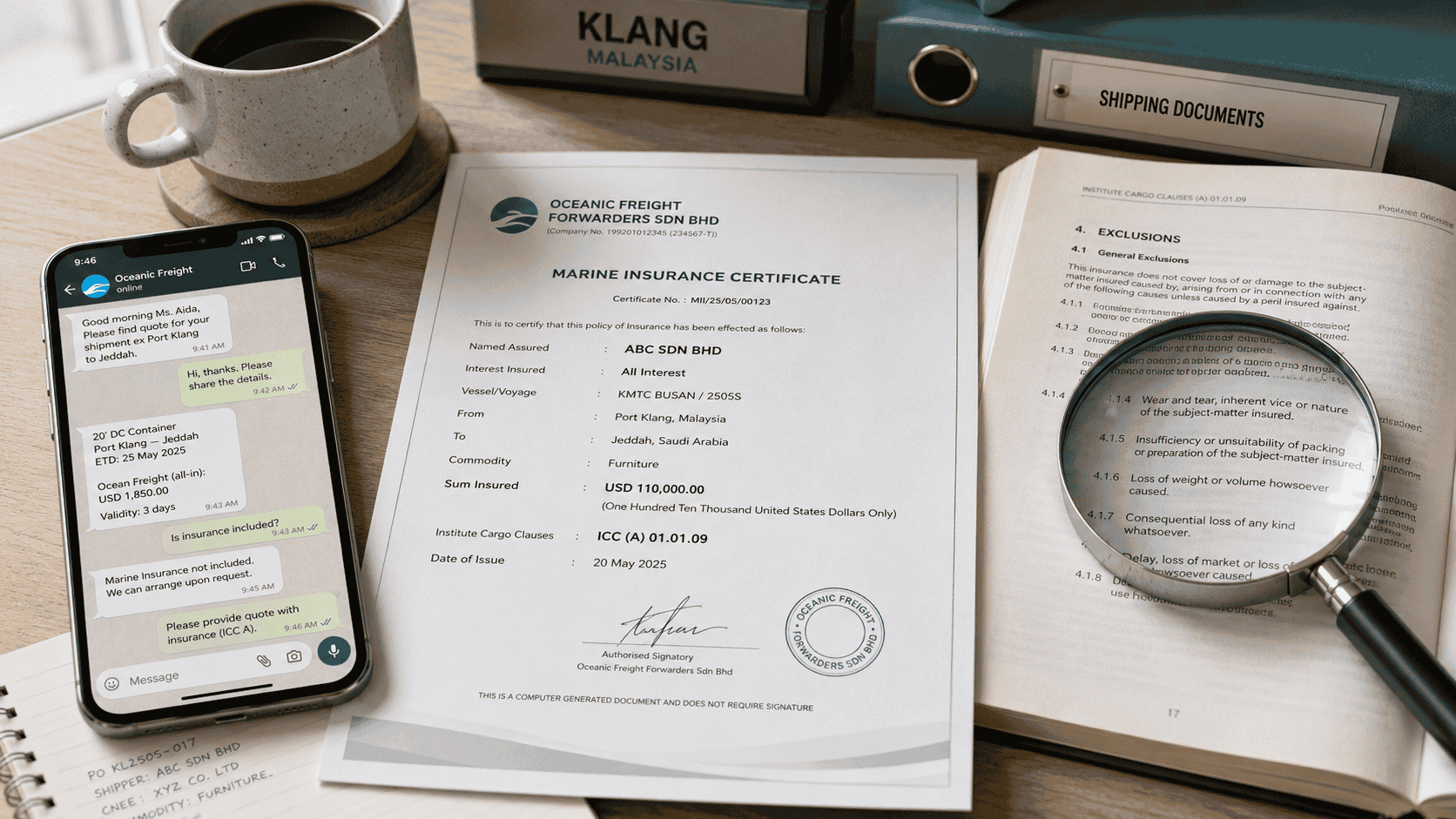

Before you change anything, read the certificate you currently hold. Several items should be checked on the face of the document, regardless of insurer.

| What to check | What it should say |

|---|---|

| Named Assured | Your company (or you, with assignment to a named buyer) |

| Sum Insured | Your shipment's CIF value plus the agreed uplift, in the right currency |

| Voyage description | The actual transit, including any inland legs at origin and destination |

| Cover form | "ICC (A) 2009" if you want all-risks; "ICC (B)" or "(C)" is named-perils only |

| War risk | "Institute War Clauses (Cargo) CL385" referenced if the routing requires it |

| Strikes risk | "Institute Strikes Clauses (Cargo) CL386" referenced |

| Survey Agents | Named in the certificate, with contact details |

| Claim payable at | Where the claim will be paid (currency, location) |

| Insurer name | The underwriter behind the master cover, not just the forwarder |

If any of those is missing, wrong, or unclear, the certificate is not necessarily worthless, but you have a question to put to your forwarder.

For LC trades the bar is higher. The LC's insurance document clause will usually require: minimum sum insured of CIF or CIP value plus 10% (per UCP 600 Article 28(f)(ii)), the LC currency, cover effective no later than the date of shipment, and specific clauses referenced.

A forwarder MOC certificate that does not satisfy those requirements will be flagged as a documentary discrepancy by the LC bank, regardless of whether the cover is otherwise sound. See LC insurance certificate requirements for the detail.

When the Forwarder MOC Is Adequate, and When It Is Not

The professional read is not that forwarder MOCs are inferior to standalone policies as a category. They are not. A well-structured master cover with a credible underwriter, on ICC (A) terms, with war and strikes included, with reasonable per-shipment limits, can be perfectly serviceable for the cargo owner.

The factors that push toward "adequate" are:

- Standard commodities not on the master cover's exclusion list

- Shipment values comfortably below the per-shipment and per-conveyance caps

- Trade routes within the master cover's territorial scope

- ICC (A) form referenced

- War and strikes included where the corridor warrants it

- Routine LC requirements that the certificate format can satisfy

The factors that push toward "inadequate, get your own policy" are:

- High-value shipments at or above the per-shipment cap

- Commodities on the master cover's exclusion list or attracting warranties

- LC trades where the certificate must satisfy specific UCP 600 Article 28 requirements (currency, beneficiary, named clauses) the master wording is not built to handle

- Trades on older or non-classed vessels not covered by the Classification Clause without notification

- Goods needing storage extension at intermediate locations beyond the standard transit clause windows

- Routing through Joint War Committee listed areas where war risk pricing and cancellation terms are commercially material

- Project cargo, specialist or high-value transit, or stock throughput exposures that need specialist wording

The practical answer for many cargo owners is a hybrid: a forwarder MOC for routine low-value shipments, and a marine cargo open cover or single shipment policy in the cargo owner's own name for the shipments where the MOC limits would bite.

Frequently Asked Questions

Is a forwarder's marine certificate "real" insurance?

Yes. The certificate is issued under a real marine open cover with a real underwriter, and the cargo owner is the assured (or beneficiary) for the specific shipment listed.

The substantive question is whether the cover terms in the master wording match the cargo owner's needs, not whether cover exists. Always verify the certificate names the actual underwriter (not just the forwarder) and references a specific cover form.

Can I rely on a forwarder's MOC certificate for a Letter of Credit shipment?

Sometimes, but check the LC's insurance document clause carefully against the certificate. The LC will typically require minimum sum insured of CIF or CIP value plus 10% per UCP 600 Article 28(f)(ii), the LC currency, cover effective no later than the date of shipment, and specific clauses (often ICC (A) plus war and strikes) referenced. Forwarder certificates sometimes default to a different currency, a lower sum insured, or a more restrictive cover form than the LC requires.

Why does the certificate name the freight forwarder rather than me?

It typically does not. A properly issued certificate names the cargo owner as the assured for the specific shipment, with assignment to the consignee or LC bank where required.

The freight forwarder's role is as policyholder of the master open cover, not as named assured on individual certificates. If the certificate names the forwarder and not your company, ask your forwarder why before relying on it.

What happens to my certificate if the forwarder's master cover is cancelled mid-year?

Cover already attached on shipments declared before the cancellation continues to its natural termination under the transit clause. Cover for future shipments under the same master cover ceases. If you depend on the bundled cover for an ongoing programme, you would need to arrange replacement cover for upcoming shipments, which is a meaningful operational risk, particularly given that war and strikes risks under the standard Institute Clauses are cancellable on 7 days' notice (or 48 hours for US shipments).

How do I find out what is in the master open cover behind my certificate?

Ask your forwarder for a copy of the master wording. They may share it in full, provide a summary of key terms, or decline.

If they decline, that is itself useful information. A standalone policy in your own name avoids the question entirely; you have direct access to your own wording.

Are forwarder MOC premiums marked up over the underlying rate?

Often, yes. Insurance premiums are typically bundled into a freight quote and can include a forwarder margin over the underlying premium charged by the underwriter.

The actual underlying premium can be lower than what is charged to the cargo owner. A direct quote from a marine broker or specialist platform sits closer to the underlying premium because the placement is direct.

What if my goods are damaged and the forwarder is unresponsive on the claim?

Contact the survey agents named on the certificate directly, and contact the underwriter named on the certificate. The cargo owner's rights against the underwriter under the certificate do not depend on the forwarder's cooperation. A specialist marine broker can also assist with claims handling under any policy, MOC certificate or otherwise, including making sure the cargo owner meets the procedural obligations in the master wording (a typical MOC wording will include language to the effect that failure to comply with claims requirements will prejudice the claim).

Voyage Conclusion

A forwarder's marine certificate is not a non-cover document. It is real cover, on real terms, with a real underwriter behind it.

It is also cover on the forwarder's terms, not yours, and the differences become material when the cargo profile, shipment value, commodity type, or LC requirements push beyond what the master wording was built to handle. The professional move is to read the certificate, ask for the underlying wording where it matters, and compare against what a policy in your own name would look like.

Voyage places marine cargo open covers and single shipment marine cargo insurance directly in the cargo owner's name, with the cover form, sums insured, war and strikes scope, and commodity terms negotiated against the cargo owner's specific trade programme rather than bundled into a forwarder's portfolio. We can quote on a comparison basis against your existing forwarder MOC, so the structural differences are visible side by side. For industry segments where MOC commodity exclusions commonly bite, see commodities and trading houses and manufacturing and industrial exports.

For freight forwarders looking at this question from the other direction, see freight forwarder's liability insurance. Reach us via the contact form or WhatsApp.

Disclaimer: This article provides general guidance on freight forwarder marine open cover certificates as of May 2026. References to specific MOC provisions are illustrative of typical Malaysian-market wordings; individual insurers' wordings vary materially. Coverage terms, conditions, and availability vary by insurer, policy, and jurisdiction.

Regulatory requirements differ between markets and may change.

Always review your specific policy wording and consult a qualified insurance or legal professional before making coverage decisions.

Why Voyage

Marine Insurance Specialists

International Underwriter Access

Both Sides of the Supply Chain

Malaysia and Singapore Expertise

Other industries

Explore other industries we cover

E-Invoicing for Freight Forwarders in Malaysia: LHDN Phase 4 Compliance, RM10,000 Rule, and MyInvois Guide

Learn more

Get Best Rates / Quotation

Voyage is a specialist marine insurance intermediary arranging marine cargo and marine liability coverage for businesses in Malaysia, Singapore, and internationally. All insurance is placed through licensed broking partners.

Riskflow Sdn Bhd (202101001225):

Suite 3.19 (North Block), The Ampwalk, 218 Jalan Ampang, 50450 Kuala Lumpur, Wilayah Persekutuan Kuala Lumpur

t: +60149255243 (Kevin H.)

email: kevin@voyagecover.com